How to apply for an HDB BTO

Getting a Build-To-Order (BTO) flat in Singapore can be a tedious process. There are a bunch of choices to be made, documents you need to submit, and payments that need to be done, and it can all get very confusing – so here’s a breakdown of the 13-step process to guide you through the journey of a BTO application:

Table of Contents

– Pre-application –

Buying an HDB BTO flat to call your own is a sure mark of adulting, but there’s much to settle before you even kickstart the BTO application process and religiously scout out flat launches to ballot for.

If you’re scratching your head upon hearing terms like “stamp duty” and “joint singles scheme”, it’s best to familiarise yourself with these things before you go on a mission to find your dream BTO unit.

1. Check out the quarterly flat sales launch

Upcoming BTO project in Tengah.

Image credit: HDB

BTO flats are released four times a year, typically around February, May, August and November. As a head’s up, HDB will announce the launch six months prior on the HDB Flat Portal, with a preview of upcoming launch details – including a map of the area and types of units available. You can use this preview time to decide if you’d like to apply for the flats that are open for sale.

The number of vacancies available varies between launches, but there are usually several locations up for grabs, spread across both mature and non-mature estates.

2. Check the eligibility criteria

Here are some nitty-gritty details to take note of to check whether you’re eligible to apply for a BTO:

Citizenship: Whether you’re planning to live with your partner or your folks, at least 1 of you has to be a Singapore Citizen and 1 more member has to either be a citizen or a Singapore Permanent Resident (PR). The other occupants can be non-residents.

While first-timer households that consist of 1 Singaporean and 1 or more PR must pay $10,000 to purchase a flat, the Citizen Top-Up Grant will provide $10,000 once your spouse or child gets Singapore citizenship.

Age: All applicants have to be at least 21 years old. If you or your fiance/fiancee are between 18 and 20 years old, written consent is needed from the parents or guardian before the flat selection appointment.

Income: HDBs differ in their income ceilings, which is the maximum combined income you and your co-applicant can have. Depending on specific BTO projects and the estate you’re going for, a general guide is $7,000 for 2-room Flexi flats, $7,000 or $14,000 for 3-room flats, and $14,000 or $21,000 for 4–room flats and bigger.

Property ownership: In order to qualify for a BTO flat, you have to be able to tick these three statements off your list:

- You do not have any other property and have not sold any property 30 months before the HDB Flat Eligibility (HFE) letter application. This includes overseas and local residential properties – both public and private.

- You have never bought more than 1 HDB, Design Build and Sell Scheme (DBSS) flat or Executive Condominium (EC).

- You have not received more than 1 CPF Housing Grant.

While most people may think of BTOs as a home for soon-to-be newlyweds, there are actually many other kinds of people you can share a HDB flat with including your siblings and BFFs.

Fiance/Fiancee scheme – For couples

For those engaged, you’re probably looking for a home before you get married. You can apply for a BTO prior to being married, but in order to collect your keys after the flat is built, you have to be legally married by the Registry of Marriage (ROM).

All you have to do is submit a photocopy of your marriage cert to the HDB Sales Office or your managing HDB branch within 3 months of your key collection. In certain cases, you can collect your keys before you get your ROM cert if you have proof of an upcoming wedding – such as a wedding banquet booking invoice.

The average waiting time to get a BTO is around 4 years, so if you’re looking to start a new chapter as a couple ASAP or are rushing to have kids, you might want to skip the wait and go for a resale flat instead. Find out how our writer got her resale flat in less than 6 months.

Public scheme – With your parents, spouse or children

Families looking for an upgrade to a new neighbourhood for better convenience can apply for a BTO together – you can either apply with your parents and siblings, or with your other half and kids. The eligibility criteria are pretty much the same as for couples.

Orphans scheme – Siblings

If your parents have passed on, you and your siblings can apply for a BTO flat together. Do note that at least one parent has to be a Singaporean or PR, and all applicants have to be unmarried, divorced or widowed to qualify for this scheme.

Singles scheme – Singles, widowers & divorcees

It’s pretty well-known that the minimum age for singles applying for a BTO in Singapore is at least 35 years old. You’re eligible as long as it’s your first BTO application. The rest of the rules – being a Singapore Citizen and having your salary capped at $7,000 – also apply.

Do note that singles eligible are only able to apply for a 2-room Flexi flat in non-mature estates.

Non-resident scheme – Foreign husband/wife

First-timer applicants with a spouse that’s not a Singaporean or PR can apply for a new 2-room Flexi flat in non-mature estates, namely areas like Woodlands and Bukit Batok that have been around for less than 20 years. Do ensure that your spouse has a valid Visit Pass or Work Pass to qualify.

You, as the applicant, must also be at least 35 years old, and both of you must have a combined income of no more than $7,000.

Joint-Singles Scheme – Friends

Round up a maximum of 3 other single kakis to apply for a new 2-room flat in a non-mature estate of your choice. All co-applicants have to be Singapore citizens and at least 35 years old.

3. Know more about the types of HDB BTO flats you can apply for

Image credit: HDB

What’s a 2-room Flexi and how is it different from a regular flat? Who can apply for a 3Gen flat? Which categories can singles apply for? These are some questions you might have if you’re a complete newbie to the public housing options in Singapore.

For the benefit of those who are 100% clueless, here’s a guide to the different types of HDB BTO flats in Singapore, with details like flat size, prices, and who can apply for them all nicely laid out.

Before we delve into the details, note that the category of a certain type of flat does not denote the number of bedrooms; A 3-room flat does not have 3 bedrooms, but rather, 2 – this is because HDB considers the living room as a “room” in itself. In general, all flat categories come with 1 less room than in the title – apart from 5-Room flats, which only have 3 bedrooms. Don’t let the names confuse you!

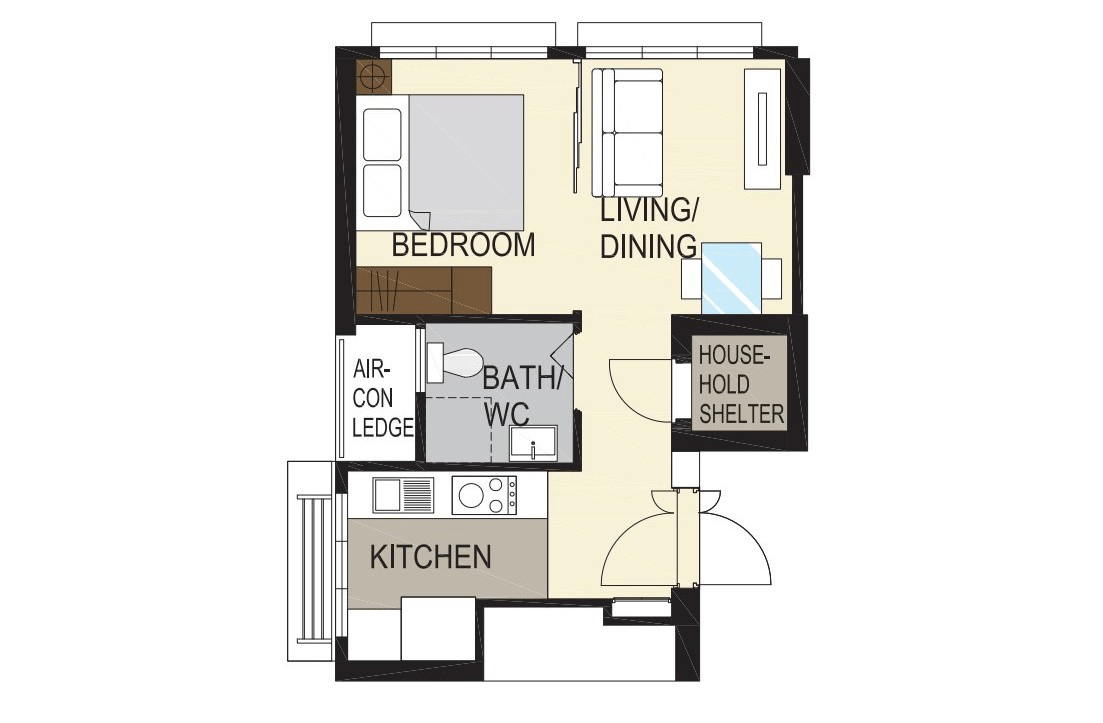

2-room Flexi flat

Image credit: MyNiceHome

Image credit: MyNiceHome

2-room Flexi flats are named as such because of the flexible lease periods extended to seniors aged 55 and above. Typically, HDB flats come with a 99-year lease, but it wouldn’t make sense for old folks to go with such a long lease when they’re probably going to be using less than half of it. Assuming you purchase a new flat at the age of 65 and you live till 100, that’s just 35 years, which is a waste, really.

This flexibility is available to elderly couples, siblings, or singles as long as all applicants are at least 55 years old, with lease periods between 15 to 45 years – so long as it covers the occupants up to the age of at least 95 years. The lease period also has to be selected in increments of 5 years (eg: 15, 20, 25, etc), which means you cannot pick a non-standard number like 32.

This is a good option for those who find a larger flat unnecessary after their children have moved out and wish to downgrade to a smaller-sized apartment in old age. A smaller space is easier to clean, and more convenient to move about in – an important consideration when you’re old and less able-bodied.

A significant portion of 2-room flat spaces are usually reserved for the elderly, and some launches are reserved solely for these aged folks. Eligible seniors must not exceed the monthly household income of $14,000.

Image credit: MyNiceHome

However, families and singles can also apply for certain 2-room Flexi flats on a 99-year lease. This is an affordable option for low-income families with a monthly household income of no more than $7,000, as well as newly-married couples who wish to save up first before upgrading to a larger flat after having kids.

Do note that the 2-room category is the only BTO category in which singles can apply. You can do so alone or under the Joint Singles Scheme with up to 3 other friends (maximum 4 people). All of you have to be single Singapore Citizens of at least 35 years old (unmarried, divorced, or widowed), and all are to be co-applicants.

If you cross the income ceiling as a single, you will have no choice but to apply for a resale flat instead.

Image credit: MyNiceHome

Image credit: MyNiceHome

A 2-room Flexi flat comes with:

- 1 bedroom

- 1 bathroom

- Living/dining room

- Kitchen

- Storeroom/bomb shelter

Floor space: 36sqm or 45 sqm

Income ceiling: 99-year lease: $7,000 | Short-lease (15-45 years): $14,000

Price: From $41,000

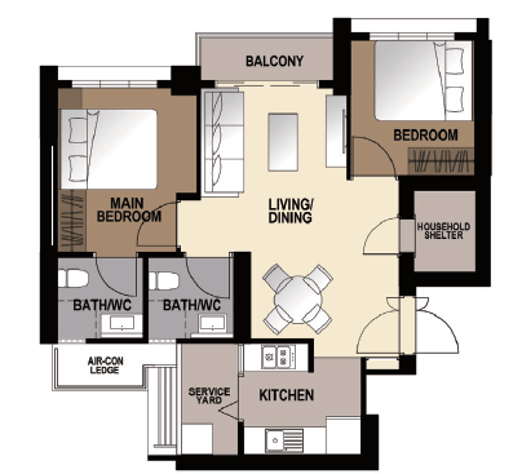

3-room flat

Image credit: Uchify

A 3-room flat is ideal for those who want to start small, with the option to sell off the flat after 5 years and move to a bigger space after amassing their wealth. It also offers a cosy space for couples with no kids and small families with just 1 child.

If you’re planning on having 2 or more kids and finances are not an issue, you might want to reconsider this option for a larger flat. A 3-room flat comes with 2 bedrooms, one of which is the master bedroom. This leaves you with only 1 room for the children. If your second child isn’t the same gender as the first, sharing a room as they grow into their adolescent years will come with some privacy issues if you purchase the flat with the intention of staying long-term.

Image credit: MyNiceHome

A 3-room flat comes with:

- 2 bedrooms, including 1 master bedroom with attached bathroom

- Kitchen

- Living/dining area

- Common bathroom

- Service yard

- Storeroom/bomb shelter

Floor space: 60-69 sqm

Income ceiling: $7,000 (non-Mature) or $14,000 (Mature)

Price: From $188,000

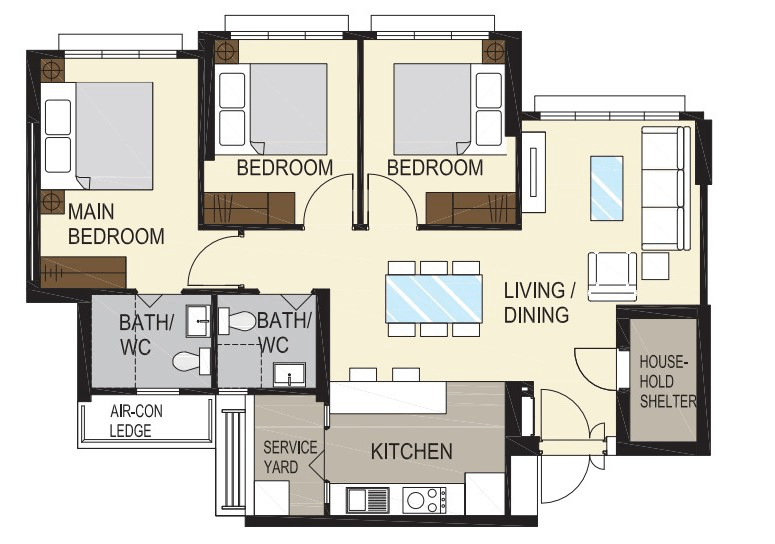

4-room flat

Image credit: Uchify

The most popular BTO flat option is the 4-room flat, and it’s just as well that there are usually the most number of such units in a given flat launch. It’s a good choice for families – whether it’s couples with a few kids or those living with their parents. Any remaining bedrooms can be turned into a study room, home office, walk-in wardrobe, or entertainment zone.

Image credit: MyNiceHome

A 4-room flat comes with:

- 3 bedrooms, including 1 master bedroom with attached bathroom

- Kitchen

- Living/dining area

- Common bathroom

- Service yard

- Storeroom/bomb shelter

Floor space: 90-100 sqm

Income ceiling: $14,000, or $21,000 if purchasing with extended or multi-generation family

Price: From $253,000

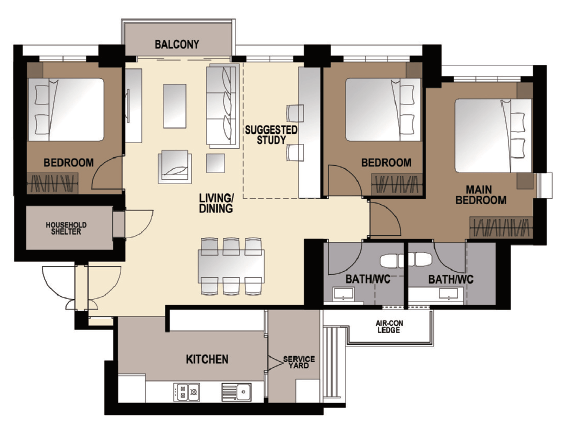

5-room flat

Image credit: Uchify

Image credit: Uchify

Before you jump to the decision of buying a 5-room flat, it is worth noting that moving up to this category will not get you an additional bedroom compared to a 4-room. However, depending on the project, you will get additional floor space of around 15-20 sqm, and this may include a balcony.

The additional floor space is distributed amongst the 3 bedrooms and the living room. This may give you the option to section off part of the living room to create a little study area or some in-built hidden storage.

Not all 5-room flats come with a balcony, so if that is something you’re adamant on, make sure you properly check the details of the project you’re eyeing before bidding.

Image credit: @juzowl via Instagram

While the thought of having a mini garden or romantic al fresco dinners in your own home sounds super appealing, remember that having a balcony requires some maintenance and thus can be troublesome – you’ll need to constantly clean the area to make sure dust doesn’t settle, and ensure rainwater doesn’t come in. It’s also potentially dangerous if you have young kids or pets.

A bit of extra floor space and a balcony are always good to have, but they’re a luxury, not a need. If these are things you can do without, you might want to consider a 4-room instead, as it’ll save you a whopping $150,000 or so.

Image credit: MyNiceHome

A 5-room flat comes with:

- 3 bedrooms, including a master bedroom with attached bathroom

- Kitchen

- Living/dining area

- Common bathroom

- Service yard

- Storeroom/bomb shelter

Floor space: 110 sqm-130 sqm

Income ceiling: $14,000, or $21,000 if purchasing with extended or multi-generation family

Price: From $405,000

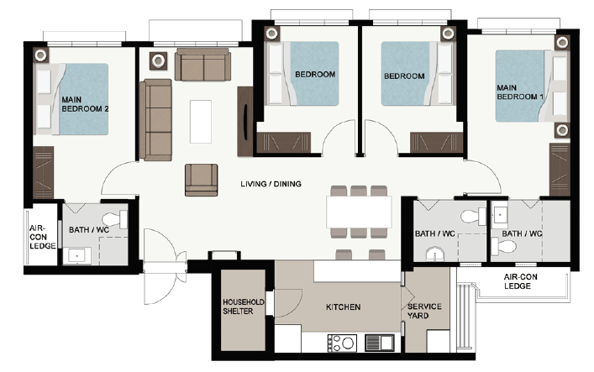

3Gen flat

Image credit: @wwwsamieme via Instagram

If you want a close-knit family unit that includes your parents or in-laws, consider applying for a 3Gen flat. With a total of 4 bedrooms – including 2 that come with attached bathrooms – everyone can have sufficient privacy while still being near each other. This is the only category of BTO flats with 2 master bedrooms, and there’s about 5 sqm more floor space compared to a 5-room flat.

3Gen flats are available to either married couples applying with their parents, or a widowed/divorced person with their child/children and parents. In both cases, at least 1 parent must be a Singapore Citizen or Singapore Permanent Resident.

One downside to 3Gen flats is that you can only sell them off to similar multi-generational families, which limits your sales opportunities.

Image credit: MyNiceHome

A 3Gen flat comes with:

- 4 bedrooms, including 2 with attached bathrooms

- Kitchen

- Living/dining area

- Kitchen

- Common bathroom

- Service yard

- Storeroom/bomb shelter

Floor space: 115 sqm

Income ceiling: $14,000, or $21,000 if purchasing with extended or multi-generation family

Price: From $457,000

Loft flats

Treelodge@Punggol.

Image credit: Superhome Design via Facebook

Loft flats are the rare unicorn versions of 5-room HDBs, and the amazing thing about them is that they come with 2 storeys. These usually cost twice the price of a regular 4-Room flat – so make sure you have loads of spare cash to splash.

These can be used as multi-generational flats, but they don’t have to be – you could just be a really well-to-do couple wanting to live the condo life without splurging extra on an actual condo.

Launches for loft HDB flats are extremely rare – the last sales launch for a Punggol location was open in 2007, with the building completed in 2010, with only 15 of such double-storey units. They’re basically the BTO equivalent of maisonettes, which are no longer being built. Some examples of these are SkyTerrace@Dawson, Treelodge@Punggol, and Punggol Sapphire.

No upcoming sales are in the talks, and one should not hold out for these lest they don’t get launched for another 10 years, if ever. Your next best alternative is to get an EC, condo, or resale loft – though a resale was reportedly sold for almost a million in 2019.

Floor space: 149 sqm

4. Budget for your BTO

Unlike the game Monopoly, buying a BTO isn’t as easy as handing over a fixed amount of cash in exchange for your dream property card. Here are some extra costs to account for:

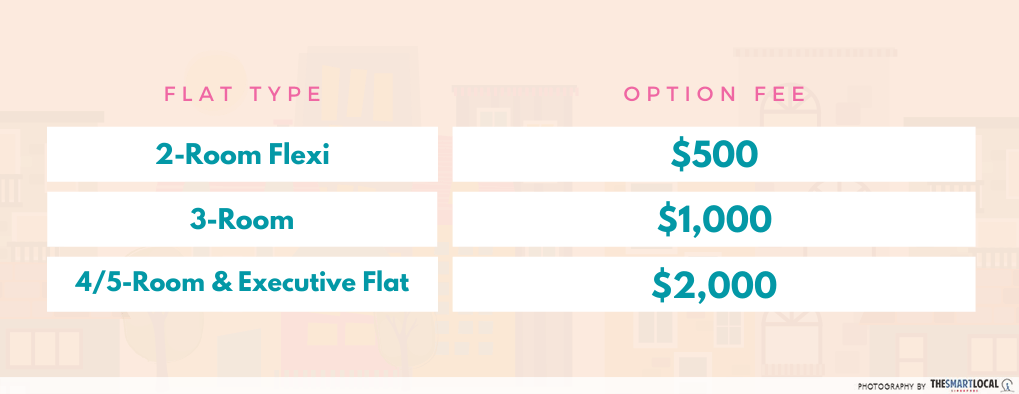

Option fee

Right off the bat, you’ve got to pay an option fee when you book a BTO flat. The amount varies from $500-$2,000 depending on the type of flat.

Downpayment

Depending on whether you take an HDB loan or a private bank loan, your downpayment due will differ. Downpayment for private bank loans starts from 25% with 5% of it in cash, while HDB loans are a fixed 20% of your BTO price that’s paid using cash and/or your CPF. The maximum amount of an HDB loan you can take out is up to 80% of the flat purchase price.

The first downpayment is due when you sign your lease agreement, so short-term budgeting is needed to ensure you have enough prior to paying for your flat. The second part of your downpayment is due during collection of the keys.

P.S. Various banks differ in interest rates, so make sure you do your research before settling for any private bank loan.

Stamp duty

Based on the price of your BTO flat, your stamp duty is paid alongside your downpayment when you sign your lease agreement. Check out IRAS’ stamp duty calculator to make things easier for yourself.

Legal fees

Let’s be honest – terms like Caveat Registration Fee and Conveyancing Fee are just big words that most of us are clueless about. Again, skip the hassle and do some quick math with HDB’s legal fee calculator.

Renovation cost

Image credit: Uchify

Finally, remember to factor in your renovation costs. Usually, this starts from $30,000 and goes up to $100,000, depending on how extensive your renovation is and what materials are used.

If you’re on a tight budget, check out these 5 HDB renovations that were done under $30,000 for inspiration.

5. Apply for a housing grant

To ease the financial burden of purchasing a house, you can apply for an HDB grant, also known as the CPF housing grant to offset the price of your BTO flat.

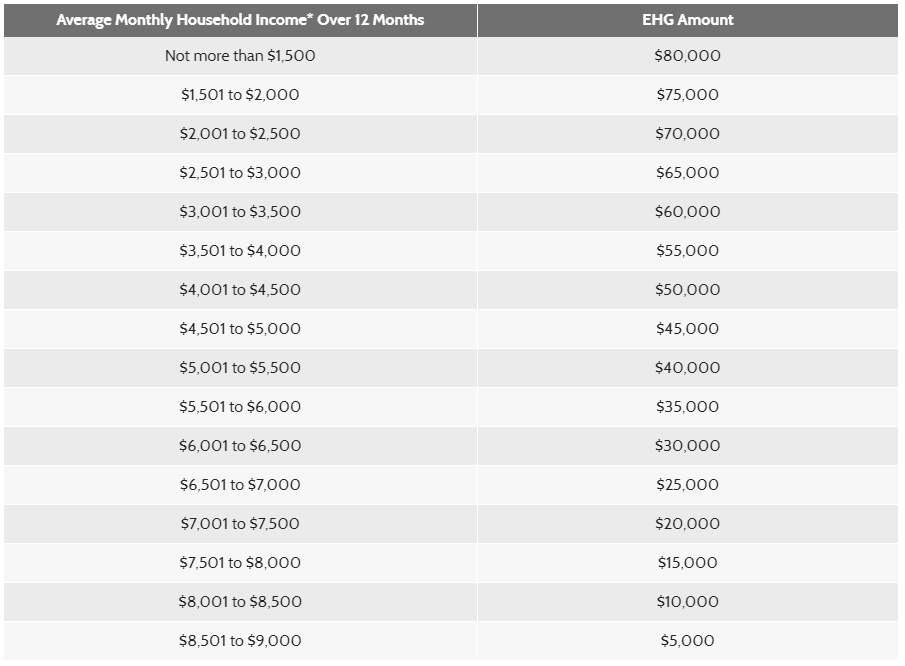

As of 11 September 2019, the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG) have been replaced with the new Enhanced CPF Housing Grant (EHG).

The grant amount ranges from $5,000 to $80,000, and how much you’re able to get depends on your average gross monthly household income for the 12 months prior to you submitting your flat application. The lower your income, the higher the grant.

EHG amount according to income.

EHG amount according to income.

Image credit: HDB

The EHG is applicable to those with a household income ceiling of $9,000 per month, for first-timer applicants. If granted, the money will be credited into your CPF Ordinary Account and deducted from there to pay for your flat.

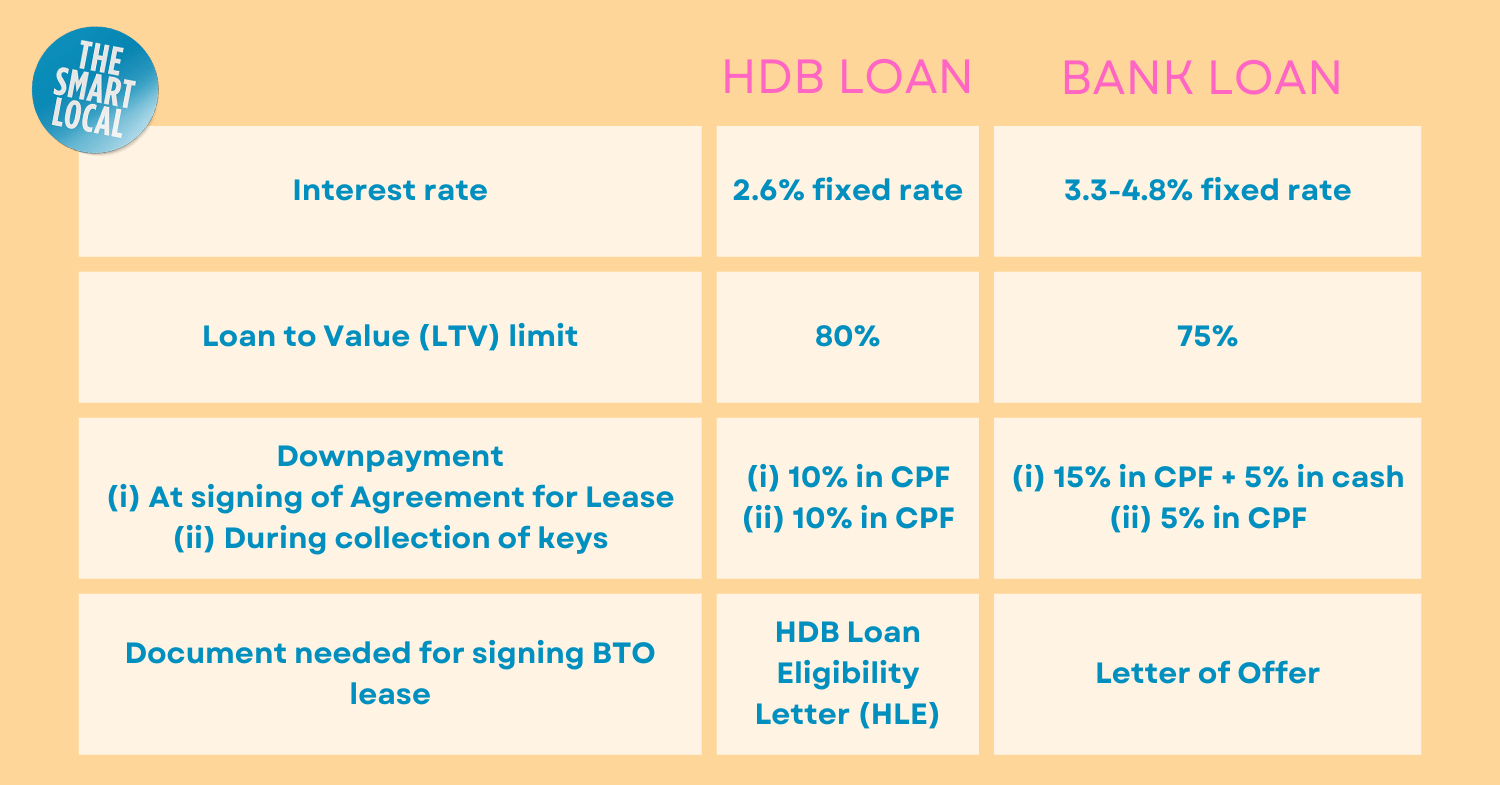

6. Explore loan options – HDB or bank loans

An average Singaporean doesn’t have several hundred thousand dollars sitting in their bank, so to pay for your BTO, you can either take up an HDB housing loan or a bank loan. Knowing the estimated housing loan you’ll be able to get will help you determine what kind of HDB to purchase.

Below are the main differences between an HDB loan and a bank loan:

Rates are as of 2023.

Rates are as of 2023.

Generally, most people prefer HDB loans to bank loans as it’s the more stable option. To qualify, you’ll need to check off the following:

- At least 1 buyer is a Singapore Citizen

- Average gross monthly household income does not exceed $14,000 for families, $21,000 for extended families and $7,000 for singles.

- No ownership of private residential properties 30 months before application for HDB Flat Eligibility (HFE) letter

The loan amount offered will be determined by your age, monthly income, and financial situation. Use HDB’s payment plan calculator to figure out the amount of payments required at different stages of buying a BTO flat.

If you’re opting for a bank loan, make sure to go to a bank that’s regulated by the Monetary Authority of Singapore. Loan amounts vary depending on which bank you go to.

– Application –

7. Apply for an HDB Flat Eligibility (HFE) letter

If you’ve been shortlisted by HDB to book a flat and are planning on taking an HDB loan, you’ll first need to apply for an HFE letter. This document gives you an overview of all your housing and financing options so you can plan your budget and make informed decisions.

Simply log into the HDB Flat Portal to apply for the letter with your Singpass. Once the results are out and you’ve got the letter, apply for an In-Principle Approval (IPA) for a loan within 6 months. Applications can be submitted on HDB InfoWEB.

8. Submit your BTO application

Commonly known as balloting, the application for BTO is the next step to securing your home. There is only a one-week window for application for each sales launch. To ensure you don’t miss it, sign up for a free alert from HDB via email and SMS notifications.

During the submission, you’ll be asked to fill in particulars such as your monthly household income. The next sales launch is in August 2023 for the following neighbourhoods: Tengah, Kallang/Whampoa, Queenstown, and Choa Chu Kang.

For those who are in more urgent need of getting an HDB flat, or are planning to stay near their parents, there are Priority Schemes that’ll help you improve your chances of getting a queue number.

Below are some Priority Schemes and who they’re applicable for:

- Family and Parenthood Priority Scheme (FPPS) – First-timer families with children below 18 and married couples below 40 years old.

- Multi-Generation Priority Scheme (MGPS) – Parents and married children applying for houses in the same estate together.

- Married Child Priority Scheme (MCPS) – Married couples who are applying for a flat within a 2km radius or in the same town as their parents.

Couples do not have to be legally married by Registry of Marriage (ROM), during the time of application, but you’ll have to submit the marriage certificate within three months of collecting your keys.

Payment required: $10

9. Wait for your balloting outcome

About three weeks after the application window closes, you’ll receive the balloting outcome. These results are computer-generated and completely selected at random, so however early or late you apply during the one-week window will not affect your chances.

If you’ve made it through, congratulations, you’re past the balloting gate! Successful applicants will get a queue number which determines how early you get to call dibs on your preferred flat unit.

– Post-application –

10. Select a unit

In order of queue number, applicants will be called down to meet an HDB officer at Toa Payoh HDB Hub 1-2 weeks after the release of balloting results. This HDB officer will guide you throughout the rest of your BTO journey.

During this appointment, there are 2 main objectives:

- Picking your preferred unit – common preferences are units on higher floors and blocks that are nearer to the MRT.

- Submission of relevant documents – Prepare your identity card or passport as well as housing loan and income documents. If you’ve qualified under certain priority schemes, extra documents need to be submitted.

Payment required: Option Fee of $500-$2,000 (by NETS)

11. Sign the agreement for the lease

Within 9 months, you can head down to sign the Agreement for Lease.

At this stage, you have more or less secured your BTO and it’s time to get down to the paperwork. This includes submitting the Letter of Offer from any bank loan or HFE letter from any HDB loan.

The ownership status of the flat has to be decided at this point as well: Would you prefer to split the share equally, and hold equal rights (Joint-Tenancy) or have the shares clearly divided, unequally (Tenancy-In-Common)?

Payment required:

- Stamp duties – IRAS’ stamp duty calculator

- Legal fees – HDB’s legal fee calculator

- Caveat registration fee – $64.45

- Conveyancing fee – $27 onwards

- Downpayment (see details in table below)

Between this and the final step, you can expect to wait an average of 3 years for the construction of your BTO. If you’ve booked a completed BTO flat, then you may get your keys within 9 months of signing the lease agreement.

12. Collect your keys

After trials, tribulations and a lot of time, you’ve reached the final step of attaining a BTO. Once HDB notifies you that your keys are ready for collection, you’ll be the proud owner of a spanking new house to call home.

Payment required:

- Balance purchase price – A combination of cash, CPF, and housing loan to complete the balance payment.

13. Get insurance and home protection post-BTO purchase

As with all valuable things, your BTO should be insured to ensure that you’re protected in case anything goes south. Below are some of the main insurance policies and protection schemes you need to look out for:

- HDB Fire Insurance – You’re automatically signed up for this when you purchase your HDB. It only insures the infrastructure of the building with premiums from $1.63/year.

- Home Insurance – Protects your home, renovation and its contents against common mishaps like burglary and damage to water pipes. It’s priced from about $53/year, and common providers include from NTUC, FWD and Aviva.

- Home Protection Scheme (HPS) – Compulsory if you are using your CPF savings to pay for your housing loan instalments. It protects you and your family from losing your HDB in the event of death, terminal illness or total permanent disability. HPS premium is calculated based on factors like outstanding housing loan on your flat, loan repayment period and percentage coverage. You can estimate the cost with the HPS Premium Calculator.

Guide to applying for a BTO flat

Phew, that was a lot to get through but it’ll all be worth it once you’re standing in your brand new BTO flat. From then on, it’s down to renovating your BTO and making it a space you’d like to stay in for years to come.

Check out more home-related articles:

- HDB bedroom design ideas

- Dark industrial design inspiration

- HDB renovation tips

- Pantone colour palettes for themed homes

- Muji-themed home decor tips

Cover image adapted from: Uchify & HDB

Co-written by Kezia Tan, Victoria Quek & Rachel Yohannan. Last updated by Aditi Kashyap on 26th July 2023.