Finance mistakes, as told by parents

Parents and nagging about money go hand-in-hand. When I entered adulthood, I thought I could finally escape them nagging me about my spending, but boy was I wrong. Turns out, it’s really because they care. And for me, it was because my mom didn’t want me to make the same financial mistakes she did.

It was a good wake up call as I was always under the impression that all had been merry and well. Looking back, I now realise my parents and many others had gone through and thankfully survived financial hardship. Here, we speak to six parents who have some sage financial advice to impart to all of us.

1. Paying for everything with credit cards

Getting a credit card is a milestone for most working adults. And while there are plenty of perks that can come with it – think airline miles and cashback – just missing one payment can snowball into a much larger problem.

For Patricia Ong, 65, one of her biggest regrets was not being careful with how she used her credit cards. The mother of four turned to paying for her family’s day-to-day necessities like food, school books, and clothes with plastic. Even though she hardly splurged on materialistic things, the cost slowly added up over time without her realising it.

“It got to a point where I would just pay off the minimum amount required, which in turn caused my credit cards’ interest rates to spike,” Patricia explained. This eventually led to her taking a loan and refinancing her home just to pay off her credit card debt, derailing her retirement plans.

“If I could turn back time, I would be more careful to pay off my credit cards in full each month and to monitor my spending,” she reflected. “I would also have invested in a retirement plan to avoid the pain of having to find work at an older age.”

2. Putting all your salary in a savings account

Us millennials and Gen Z’s have it easy with a wide selection of banking apps and robo advisors that can help us invest our money. However, according to Joanne Tan who is a mother of three, those born in the baby boomer years didn’t have the same luxury.

“Last time, all we knew was to put our savings away in our bank account to save for a rainy day,” Joanne said about her investment strategy – or lack thereof. She also felt that her CPF payout was more than enough to tide her over.

When she eventually decided to retire five years early, she had to continue to work part-time to maintain her standard of living without dipping into her savings. “I should have bought a property with tenancy early on and invested in a good insurance savings plan which would’ve given me monthly deposits earlier,” Joanne said in retrospect.

3. Having kids without proper financial planning

Welcoming a new bundle of joy into your life can be a whirlwind of emotions, and chances are you’ll just want to spoil them to the moon and back. But you might be in for a shock once you tally up all the receipts – after all, there’s that infamous saying that you need a million dollars to raise each child in Singapore.

Tim Lee, a father of two daughters in their late 20s, thought his children would have left the nest by now. “I was hoping my wife and I could finally have some freedom at home and no longer have to support them.”

This might seem like a Westernised sentiment, but no one can blame Tim’s assumption. After all, according to news reports, more millennials are moving out of their parent’s homes to live by themselves or with friends.

Nevertheless, Tim still appreciates the time spent with his daughters. After all, once they move out, their daily chatter could very well turn into just weekly or monthly catch-ups. “You have to be prepared to support them through thick and thin because they’re your blood,” Tim added.

4. Spending bonuses on big ticket items

Receiving a year-end bonus can be a rush that gets us excited about what we’re going to spend it on. A fancy new vacuum cleaner? The latest smartphone? For Matthew Chai, 58, he decided to put his bonus on a downpayment for a new car.

Having just welcomed a newborn, the father of two felt that his growing family deserved the best and swapped out his trusty Japanese hatchback for a larger SUV. But then came unexpected medical bills for his wife and kids, school fees for his eldest, and home renovation costs that slowly ate into his savings.

“If there’s anything I realised, it was how unnecessary a new car was at that time, as our old car was still running perfectly fine,” he contemplated. While he no longer drives the new car that he bought years ago on impulse, he has since been more mindful of where he channels his bonuses. “These few years I just put it into a retirement savings account.”

Check out our guide on owning a car in Singapore.

5. Getting only minimal insurance coverage to “pay less”

We all meme on our insurance agent friends who just want to “catch up.” But for Peng Leong and Peggy, they wished that they had a friend who reached out to sell them a more comprehensive medical insurance plan when they were younger. The parents of three are currently in their 60s, and the costs of old age are starting to add up.

Their current insurance policy doesn’t fully cover the hospital visits and medical appointments, and they only realised this once they had to start seeing specialists for their health issues. That’s on top of the fact that insurance premiums are higher for older folks, leading to Peng Leong and Peggy’s hesitation on getting more thorough coverage.

“We realised that just getting insurance is not enough, it’s about making sure the coverage is solid so you don’t have to pay too much in cash, too,” Peng Leong said. “It’s only in times of need like hospitalisation that you realise what you lack in insurance coverage. But it might be too late by then,” Peggy added.

P.S. Here are some good questions to ask your insurance agent before deciding on an insurance policy.

6. Living paycheck to paycheck

Not having any savings hits very differently when you’re 15 compared to when you’re 65. As a teenager, it’s easy to ask daddy and mummy for some extra pocket money. But when you’re well into your 50s and 60s, this complacency can extend your retirement by a few years.

Something that 63-year-old Jay Ng constantly tells her only daughter is to always remember to start saving for her retirement early. “I get heart pain just thinking of all the money I spent at the casino and mobile games,” she said, adding that she just wishes her 26-year-old daughter Lily would stop splurging on new K-pop merch.

Now she jokes that Lily is her “retirement plan” thanks to her successful career, but Jay also acknowledges with hindsight that her squandering has landed her in this predicament. She has since started to be more conscious of her spending habits. “There’s no point regretting, only making sure that my daughter doesn’t make the same mistakes I did.”

Planning for retirement and avoiding finance mistakes

We all make mistakes, but some may have more dire repercussions when it comes to our golden years. As these baby boomers shared, these finance mistakes can be avoided when you take long-term planning into account.

RetireSavvy, Singapore’s first flexible digital retirement product allows you to do just that. It allows you to adjust your plan whenever you want, to help you easily manage any changes later in life. Best of all, you’ll get instant approval upon application.

For fresh grads just starting their first jobs, all they have to contribute is $128.74/month* – a relatively affordable commitment. There’s also the flexibility to top-up your premium anytime after the first year, up until five years before your selected retirement age.

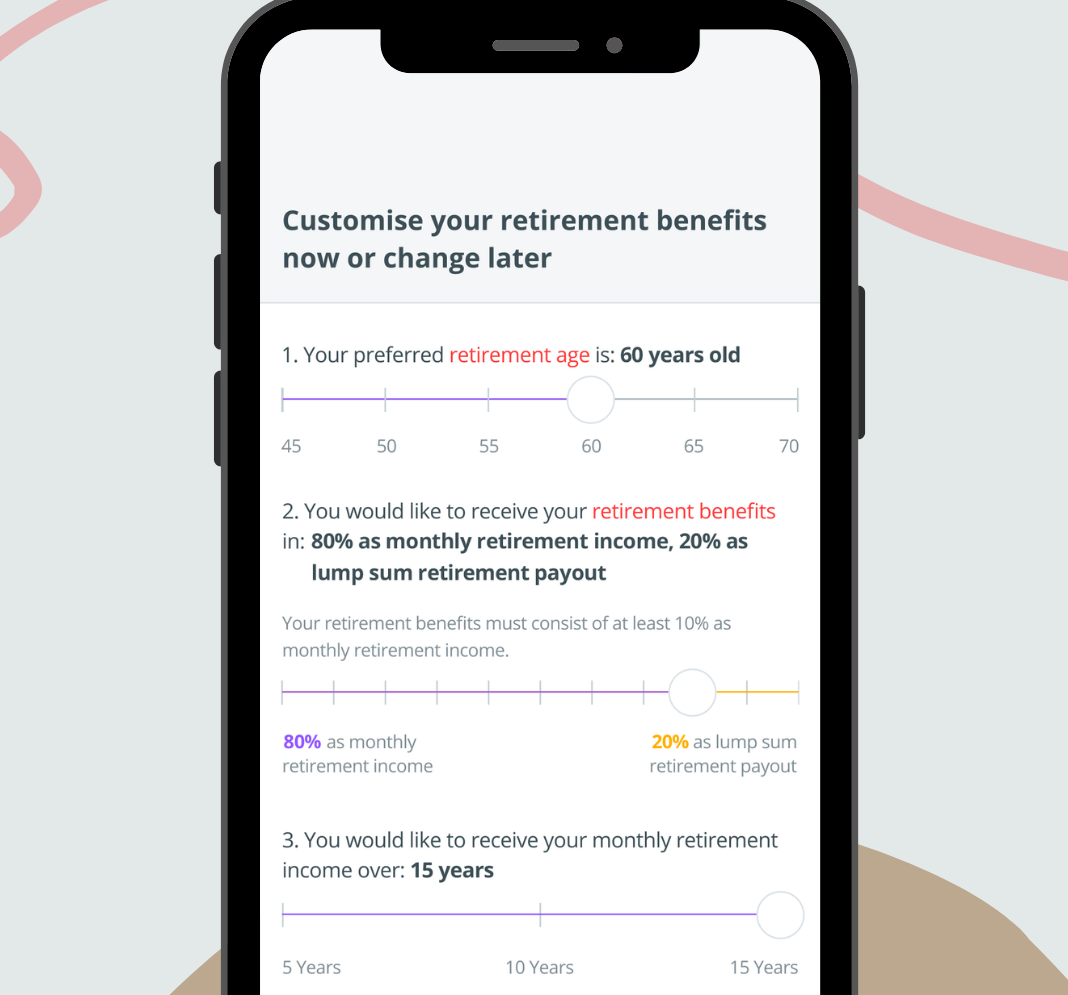

When applying for RetireSavvy, you can set the age of when you want to start receiving your money – this would be your preferred retirement age. You can always choose to defer the retirement age to a later date during the policy term if you’ve changed your mind.

Image adapted from: DBS

For example, you can retire at 70 instead of 55, and receive 20% of your retirement benefits as a lump sum pay-out, and get the remaining 80% as your monthly retirement income.

In the event of an emergency, you can put your premium payment on hold without compromising on your plan. If said emergency is a retrenchment, there’ll also be some financial protection in the form of a lump sum payout so your retirement plans don’t go awry.

With these customisable options, saving for retirement can be a priority, whether you’re climbing the corporate ladder or just a little unsure of what the future holds.

Find out more about RetireSavvy by DBS and Manulife here

This post was brought to you by DBS.