Best loan rates in Singapore

There’s a rite of passage almost every Singaporean goes through as they begin #adulting. Whether it’s marrying bae or buying a house, one thing these have in common is the need for cash. But not everybody has the moolah to finance them upfront, and in this scenario, our best choice might be to turn to loans.

That said, there’s no need to set off on a witch hunt for the best loans because we’ve already narrowed down big milestones like buying a car and house renovations, and scouted for the best ways to finance them.

1. University school fees

One of the first tastes of adulthood comes in the form of a 5-figure tuition fee. But furthering your studies is a worthwhile investment, which is why hefty school fees needn’t hold us back as there are loans to finance them.

You can opt for the CPF education scheme – aka your parent’s CPF for one of the lowest interest rates and 100% coverage of your fees. Interest rates are pegged to the Ordinary Account’s interest rate which is around 2.5% per annum.* However, this kicks in as soon as the savings are withdrawn.

But if you don’t wanna owe your parents, the MOE tuition fee loan covers up to 90% and the interest rate of about 4.75% p.a. only kicks in after your course finishes.

For those who intend to study in private universities like Kaplan or MDIS, education loans offered by banks are the only option with rates from 4.5% p.a**. And if doing your Masters is in the horizon, expect to fork out amounts over $30k, which definitely warrants a loan.

*Note: This fluctuates and is accurate as of 16 April 2019.

** Effective Interest Rate – 5.17%

2. Car

Cruising in a sweet new ride is one of life’s milestones, but beyond that, a car can be a convenient means of transportation, especially when you have kids or need to drive to work every day. That said, buying a car comes at a cost you might need a loan to finance.

You can take a loan of up to 60-70% of the valuation or purchase price of the car – which includes the car’s Open Market Value (OMV), Certificate of Entitlement (COE) and other fees, taxes and duties. The percentage of your loan amount will be based on your OMV – if it’s less than $20,000, you can loan up to 70%, if it’s more, 60%.

For example, you get a Honda Civic where the real cost of the car – aka your OMV – is $19,$370 and it totals $82,460 after adding in COE and other items. You can take a loan amount of around 70% of that ($71,399) since your OMV does not exceed $20k*.

But before you make any hasty decisions, be sure to source for the best interest rates for car loans.

As for the other 30% ($30,600*), consider taking personal instalment loan for a longer loan tenure that’ll give you more time to pay off – like over the course of 3 years.

*Based on a Honda Civic 1.6 i-VTEC. Source: SG Car Mart.

3. Wedding

So you’ve finally found your Prince Charming or Cinderella and the next step is to let the world know. But weddings can have a hefty price tag of about $60,000 when you consider things like outfits and hiring a photographer, and if you’re strapped for cash, a loan might be your best bet.

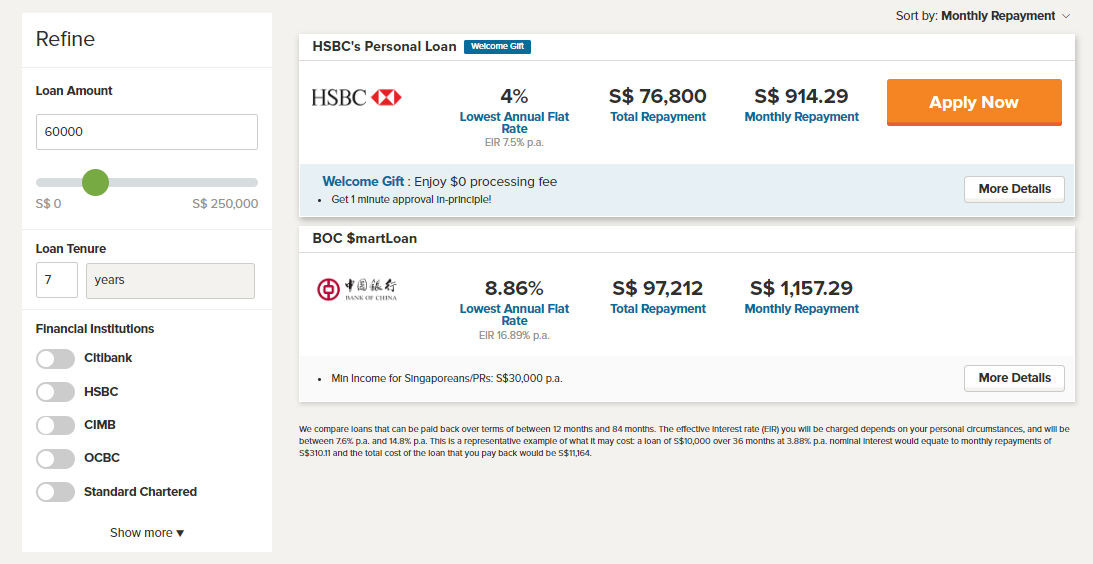

For large loan amounts, consider HSBC’s Personal Loan which allows you to borrow up to 8x your monthly income and with the longest loan tenure of 7 years.*

*If your annual income is >$120k.

If you fall within a lower income bracket, most banks limit the borrowing amount to 4x your monthly income. Assuming that you earn $4,000 per month, you can borrow up to $16,000 to finance part of your wedding costs.

But which bank has the lowest interest rates, you ask? Well, currently Standard Chartered CashOne Personal Loan is looking to be an attractive option with the lowest interest rate of 3.88% p.a. (EIR 7.63% p.a.) and monthly repayment of ~$320 for a tenure of 5 years.

Of course, when a wedding takes place, a honeymoon follows suit. Whether you’re headed for Santorini or the sandy beaches of Maldives, you’re gonna want to get yourself covered with travel insurance. Narrow down your search based on destination and price here.

4. Housing

The equivalent to a proposal in this day and age is – “babe, wanna BTO anot?” Plus, if there’s a BTO being developed near your parents’ house or familiar childhood estate, you might wanna ‘chope’ a spot asap since it’ll take a whopping 3-5 years to build.

To get around financing your BTO or resale flat, you can take a HDB Loan of up to 90% of the purchase price, at 2.6%* interest rate – the remainder can be paid using cash or CPF.

Image credit: Jessica Lai

Image credit: Jessica Lai

If you purchase a private property or have exceeded the combined income ceiling of $12,000 for HDB loans, it’s time to turn to bank loans. Bank loan offers the lowest interest rates and lets you borrow up to 75% of the purchase price – but 5% of the downpayment, that can come up to about $20,000 for a 5-room flat has to be made in cash.

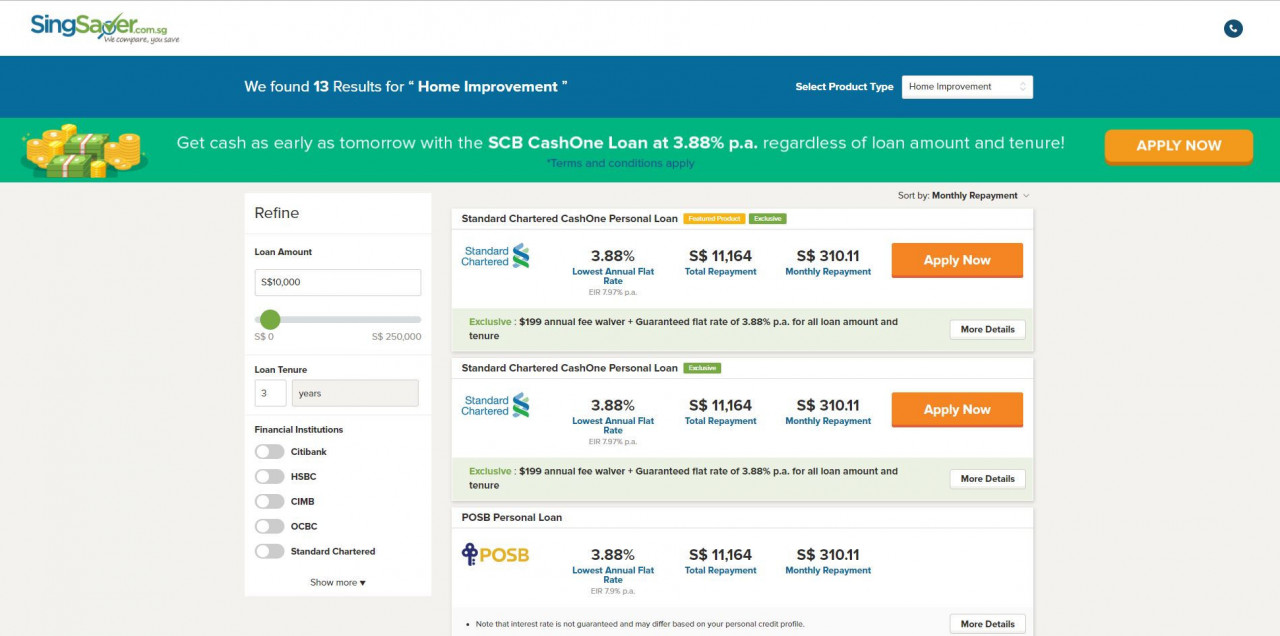

If you’re short on cash savings, consider financing the downpayment with the Standard Chartered CashOne Loan which offers the lowest guaranteed flat rate of 3.88% p.a. (EIR 7.97% p.a.), no matter how much you wish to loan or for how long – psst, this deal is exclusive to Singsaver. This means a monthly repayment of $620 for the next 3 years. Consider opting for a loan tenure shorter than the time needed to build the flat, so your debt doesn’t snowball when mortgage kicks in.

Alternatively, if you’re sure you can pay it off within a 6-month loan tenure, go for balance transfers aka Credit Card Fund Transfers, a short term loan with 0% interest and a one-time processing fee. Yes, zero interest. Fair warning though, if you don’t pay up in time, the penalty payments can be pretty high.

P.S. If you’re looking for a balance transfer, you might want to check out the Standard Chartered Credit Card Funds Transfer. Through Singsaver, you can currently get an exclusive rate where processing fee is only 0.9% of the loan amount for new cardholders.

*accurate as of 12th April 2019

5. Renovations

You’re clutching the keys to your new home in your hands, and now it’s time to wave your magic wand and turn it into a minimalist haven or a swanky boutique ‘hotel’. Whichever you opt for, renovations usually costs upwards of $30,000, which you can finance with a renovation loan.

The renovation loan on our radar is the Maybank Renovation Loan which offers the lowest monthly rest interest rate from 4.33% p.a. Do note that renovation loans are capped at $30,000 and if that won’t suffice, you can consider taking up a personal instalment loan to tie up the loose ends.

6. Baby expenses

Let’s face it, baby expenses don’t come cheap. After all, you only want the best for your little bub. Whether it’s diapers, formula milk or a pram, it adds up. Plus, when prenatal care and birth costs amount to just under $10,000 for private hospitals, your unsecured debt might increase.

Unsecured debts are debts with no assets attached to them, which means that the bank can’t claim, say, your house when you fail to pay up. And one of the most common types is credit card debt, where interest on overdue payment can stack up to a mindboggling over-20%.

Since the interest rate is so cray-cray high, one strategy is to pay off outstanding credit card bills first with personal loans or a balance transfer for longer and shorter tenures respectively.

However, if your outstanding unsecured debt is more than 12 times your monthly income, consider a debt consolidation plan that’ll consolidate everything into 1 loan with a lower interest rate*, and can cover greater loan amounts with up to 10-year tenures.

Our top pick is HSBC’s Debt Consolidation Plan offering the lowest interest rates at 4% p.a. with a 1-10 year loan tenure. In other words, you’ll spend less time paying multiple bills and more time with your kiddo.

7. Medical expenses

When you’re old and grey, your health might no longer be what it used to be which might mean more hospital visits. At the ripe age of 55, you can start to dip your fingers in and withdraw funds from your CPF which can help finance medical costs. The only catch is that you have to leave a minimum sum inside, $88,000 for property owners and $176,000 for non-property owners.

At 65, you’ll start to receive monthly payouts from CPF Life. But if the monthly payments don’t suffice, and you’re not covered by insurance, you might need to take up personal loans for your medical bills.

SingSaver helps you find the best loan rates for free

Image credit: SingSaver

Image credit: SingSaver

When it comes to the big ticket purchases in life – especially those in the 5-figure zone, loan rates make the biggest difference. Which is why it’s imperative to shop around and source for the lowest interest rates before taking up a loan.

But there’s no need to spend hours scouring through Google to compare interest rates because SingSaver helps you find the lowest loan rates at a glance. All you have to do is head to their website, choose the type of loan you wish to take up on their website and pick out the best option. You’ll even be able to apply for the loan directly on the website.

The site is also impartial and shows all interest rates available transparently – aka no favouritism for any particular bank. So, you can be reassured that you are getting non-biased info. And best of all, it’s utterly free to use the platform!

It’s really that simple, and before you know it, you’ll be in your shiny new car or living it up in your freshly renovated house with the assurance that you’ve bagged the best deal.

Find out more about the best loan rates here

This post was brought to you by SingSaver.