CPF contribution in Singapore

One of the surest signs of adulting is perhaps when you start probing dutifully into how CPF affects you, rather than just through some uncle’s rant about how his money is being “unfairly locked up”.

Truth is, CPF, or the Central Provident Fund, is the government’s way of auto-imparting the virtue of thrift in each of us – to help us save up now and enjoy the fruits in our golden years.

Trying to make sense of how CPF works doesn’t have to be confusing and tedious. Here are the essentials you need to know.

CPF contribution rates

Both you and your employer need to make contributions to your CPF account. During payday every month, your employer will withhold a portion of your wage for CPF. Separately, your employer will have their own contribution, which is on top of your wage.

Your employer will then deposit the combined contribution to your CPF account on your behalf.

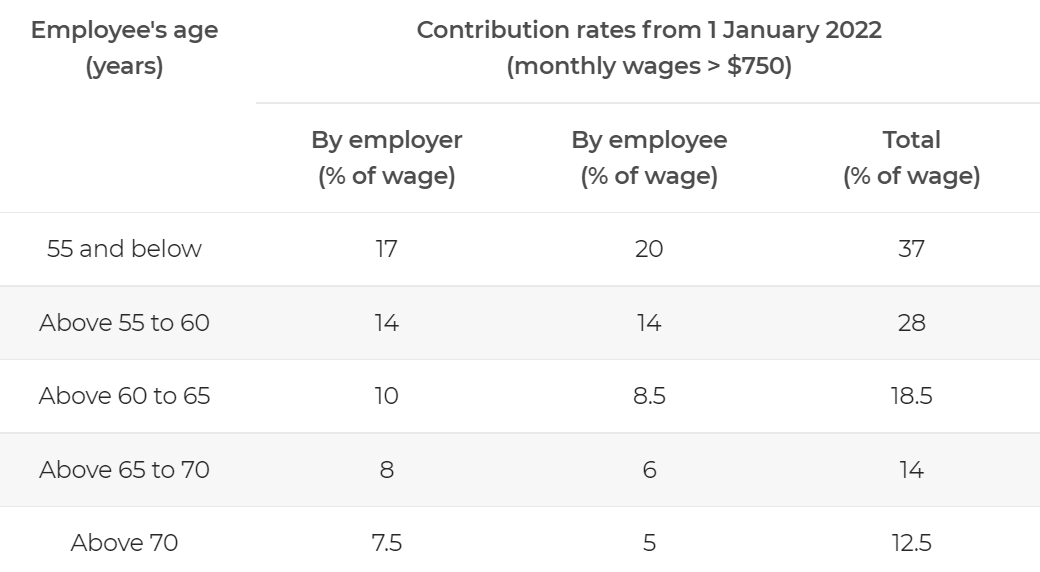

Here are the CPF contribution rates from 1 Jan 2022, for monthly wages of $750 and above:

Image credit: CPF website

For those earning below $750, the employer still has to make CPF contributions based on the rates above. But the employee’s contribution rate is tiered based on the following salary bands:

- $501-$749: 1% to 20%

- $500 and below: 0%

Payments that need CPF contributions

Bonus time? A portion of it will go back into your CPF.

Most payment types by your employer to you need CPF contributions. Examples include:

- Basic wage

- Overtime pay

- Cash incentives

- Bonuses, including Annual Wage Supplement

- Commissions

- Tips

- Allowances and subsidies, such as for housing, meals, travel, clothing, mobile phone and plan subscriptions

- Leave encashment

- Cash payment or subsidies for purchase of company stock

- Ex-gratia payments

There are certain exemptions, such as the following:

- Reimbursement

- Donations, such as for bereavement

- Insurance payouts

- Non-cash gifts and benefits-in-kind

- Cash prizes from contests

CPF contribution caps

There’re limits to how much you and your employer can contribute to your CPF, namely the Ordinary Wage Ceiling (OWC) and Additional Wage Ceiling (AWC).

Ordinary Wage Ceiling

The OWC is applicable for each month, for wages like your monthly salary, commissions and allowances.

OWC works this way: let’s say your pay for the month is $6,500. You and your employer need to make CPF contributions for only $6,000. The remaining $500 is yours to take home.

Currently the OWC is the first $6,000 of your monthly wage. But if your pay is $6,000 and below, the full amount is subject to CPF contributions.

Additional Wage Ceiling

On the other hand, the AWC is calculated on a yearly basis, for wages like annual bonuses.

There’s a fixed formula for the AWC, based on your total monthly wages for the year. CPF provides a handy tool to easily calculate your AWC.

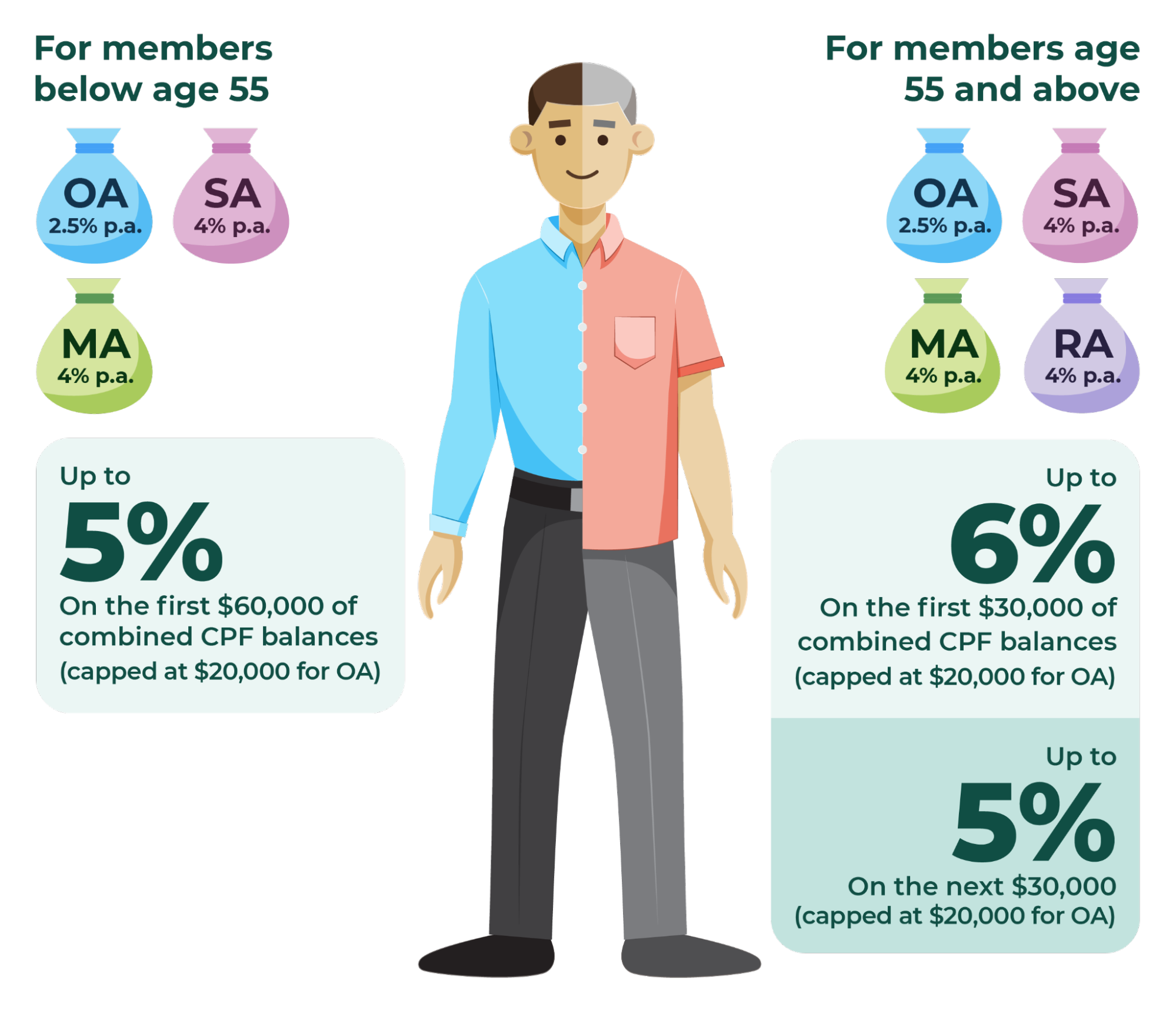

Where do your CPF contributions go?

Image credit: CPF

Fret not, your CPF contributions do not just sink into a black hole, never to be seen again. The money ends up in the following pots:

Ordinary Account (OA):

The OA can be used for major life needs such as buying a house and paying off higher education loans. With a yearly interest rate of 2.5%, it helps to beef up your money against mortgage and other lending rates, as well as inflation in general.

Special Account (SA):

The SA is meant as a longer-term nest egg for your retirement. Which explains the higher interest rate of 4%.

MediSave Account:

MediSave is your healthcare kitty, supporting larger medical expenses like hospitalisation and selected outpatient treatments. It is also used for medical insurance premiums, and carries an interest rate of 4%.

When can your CPF money be withdrawn?

Your MediSave savings cannot be withdrawn in cash no matter your age. When you pass on, it will go to your next-of-kin in cash, based on your CPF nomination or Singapore’s inheritance laws.

Your OA savings can also be used when buying a house.

For your OA and SA savings, you can withdraw them in cash from age 55, subject to a minimum Basic Retirement Sum (BRS) if you own a property or Full Retirement Sum (FRS) if you do not own a property.

The BRS and FRS are to make sure you have enough money for retirement after age 65, and will be disbursed to you in monthly payouts after that age.

The table below gives you an idea of how much is set aside for your BRS or FRS, depending on when you turn 55:

Image credit: CPF website

Hence, once you hit 55, you can cash out any balance above your BRS or FRS, with a minimum withdrawal of $5,000.

Can you invest your CPF money?

Attractive interest rates are not the only way to grow your CPF savings. You can also invest any balance above $20,000 and $40,000 in your OA and SA respectively.

Your investments need to go through selected local banks such as DBS or other local-based financial institutions like insurance companies and fund managers.

A wide range of investment products is available, from unit trusts, investment-linked insurance policies to endowment plans and Singapore government bonds. That said, the products have been pre-screened to weed out excessively risky ones.

Again, withdrawing your CPF investments is only allowed after age 55, subject to your BRS or FRS.

Which employees are exempt from CPF contributions?

For the vast majority of employees in Singapore, CPF contributions are compulsory.

There’re a few exceptions though, like the following:

- Singapore citizens (SCs) and permanent residents (PRs) on long-term overseas postings, not including short-term assignments like business trips, conferences, training.

- Foreigners who are not SCs and PRs.

- Domestic helpers who do not work more than 14 hours per week.

- Students who meet exemption criteria, e.g. government-school students working during official school holidays.

- Employees of United Nations organisations and agencies.

- Seamen working on Scandinavia-registered ships.

If you are self-employed, including as a freelancer, contributing to your OA and SA is optional, since you are not considered an employee. However, Medisave contributions are still compulsory if you earn more than $6,000 a year.

How to check your CPF contributions?

You can easily check your CPF contributions for the past 15 months and account balances via the CPF website or app, using your Singpass.

Your employer needs to make CPF contributions by the 14th of each month, for the previous month’s work. If there’re any discrepancies, such as underpayment or non-payment, you should approach your employer.

Alternatively, you can lodge a report with the CPF Board.

Growing your nest egg

Like it or not, CPF is an inseparable twin of working life in Singapore for most of us.

You may feel the pinch, seeing a chunk of your salary “locked up” every month. Still, it’s a tried-and-tested way of growing our finances in a disciplined manner, one that helps take care of major life needs and old age.

More articles for those starting out: