Biggest investing mistakes beginners should avoid

Besides forming newfound independence, a major part of adulthood is becoming financially stable. A good start is setting aside your savings for a retirement plan. But to get your money working for you, investing is one way to bring in some passive income.

Starting on your own can be intimidating, especially when the returns are left to the hands of fate. But if you want to start investing with a 10/10 plan, follow where others have gone and thrived. We spoke to financial and investment advisors to find out the six biggest investing mistakes you should avoid if you’re a blur beginner:

1. Failing to diversify your portfolio

It’s near impossible to find the perfect investment as each comes with its own set of risks. But once you find one you’re interested in, “a common mistake is to put all of your eggs in one basket by investing all of your money in that single investment,” shared Robin, a former financial advisor.

He explained, “there’s no guarantee over which investment will do well or flop”. As such, consider channelling your funds into different types of investments to minimise stock-specific risks, such as index funds or Exchange Traded Funds (ETFs). This basket of assets will at least prevent drastic losses.

To keep tabs on your different investments on the reg, consider using a digital investment service like ProsperUs. They have access to multiple asset groups, such as stocks, bonds, and funds across global markets.

2. Letting your emotions affect your decisions to buy or sell

Unless you’re a robot, it’s likely that sometimes emotion drives your decisions. But when it comes to investments, it’s important to manage your impulses.

Robin warned that “many new investors get entangled in media hype or fear”. He shared how many of his friends sank their savings into cryptocurrency for fear of missing out on profits, then sold their tokens at a loss when the market crashed.

To manage emotional impulses from following the market’s ups and downs, he suggests applying the Dollar Cost Averaging (DCA) approach to investing. This involves putting a set amount of money in the same stock or ETF over a period of time regardless of its market performance.

Doing this averages out the price you’ll pay for a bond or stock over the long run, rather than sinking in all your money in one go at a potentially high buy-in price.

3. Not paying attention to hidden fees in investment apps

Heads up if you often skip reading the T&Cs and just blindly click ‘accept’. Susan, a financial advisor, says that this is one of the easiest ways new investors lose a few dollars from their bank account monthly without their knowledge.

“Make checking your bank statements a habit to see if you’re incurring service charges you aren’t aware of,” she advised. If you see small transactions from an investment platform here and there, you might want to check what these charges are for.

“Many digital investment services will charge additional fees, like commissions and trading fees for actions as simple as transferring money,” she said.

While the fees may not cost you a fortune, it’s still important to keep tabs on how much these platforms are charging. You might want to consider changing to a different brokerage or adjusting your investments based on these hidden fees.

4. Trying to guess when to buy and sell

Time is of the essence when it comes to investing. You ought to hold onto an investment for a certain period of time to maximise your returns. But, it can be easy for newbies to get swept up in the euphoria of trading in order to rake in large returns by attempting to time the market.

Market timing is the process of buying and selling based on up-to-date information about the financial markets in order to make a quick profit. It’s a skill that wages on risk and takes years of training to master.

Even for someone as seasoned as Aziz, an investment advisor, he cautions against playing with market timing if you haven’t assessed how much you’re willing to lose on an investment. “New investors who try to time the market quickly bail out when they misjudge normal dips or when their investment growth isn’t as rapid as they thought it would be,” he said.

Your best bet is to set realistic expectations and understand the risks involved with certain investments. This will let you know if you’re more suited for market timing or investing for the long run.

If you’re a beginner who struggles to make a good investment, it’s best to seek the advice of seasoned investors. Insights and webinars on markets that are doing well can often be found online. For those with a ProsperUs account, such resources are available for free on their website.

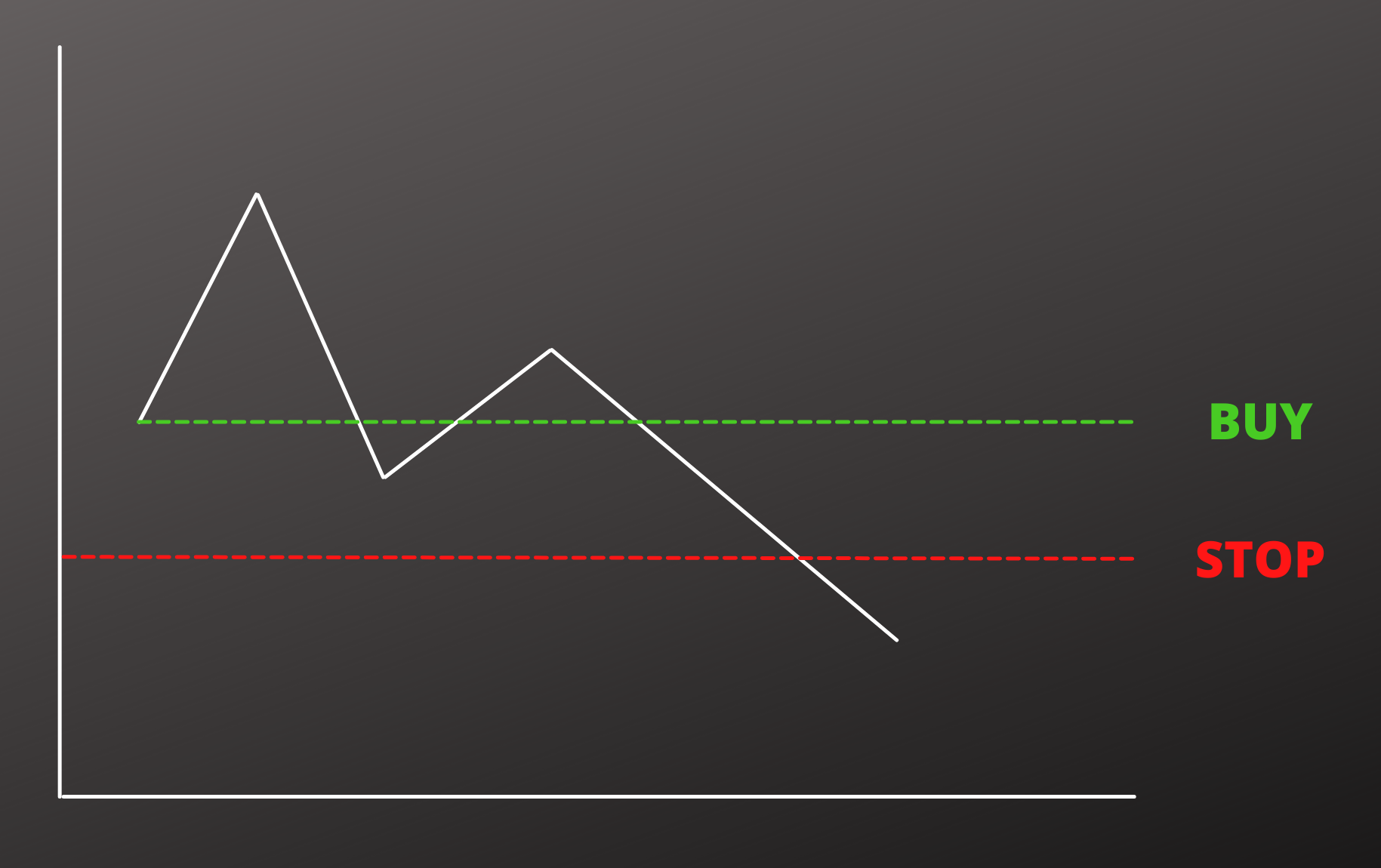

5. Accumulating excessive losses without a plan

Stop-loss order

Though losses are a normal part of investing, it’s still something you want to minimise. Thus, “having a plan can help you avoid, and bounce back quicker from excessive losses”, said Aziz. “Knowing what your risk appetite is can be reassuring when you face a dip in the market.”

To make sure you never go over the maximum level of loss, he suggests implementing a stop-loss order in your investment platform. This automated command serves to limit how much you’ll lose. At the very least, it’ll give you security in knowing the losses you make have been controlled by you.

For example, if you were to set a stop-loss order at $25/share, these shares will automatically be sold at this price once the market price hits this amount in order to help minimise your losses.

6. Not having a long-term investment plan

There’s a misconception that trading a few stocks and shares is a surefire way to rake in cash quickly. But while some investors may have lady luck on their side to give them high returns in short turnarounds, some of us may not see such profits until years later.

With this in mind, it’s best to think of investing as a long-term game plan, says Robin and Susan. As the saying goes, “slow and steady wins the race”.

But it isn’t just enough to apply principles like dollar-cost averaging and building a diverse portfolio. Seasoned investors must also know how to adjust their investments over time. For example, putting in $100 a month now won’t have the same value a few decades down the road.

Both financial advisors also emphasised understanding your future financial needs to help in planning your long-term investments. Buying a home or having kids are huge financial responsibilities that may hinder this. You might want to cash out on certain investments by then or lower your monthly deposits to accommodate new expenditures.

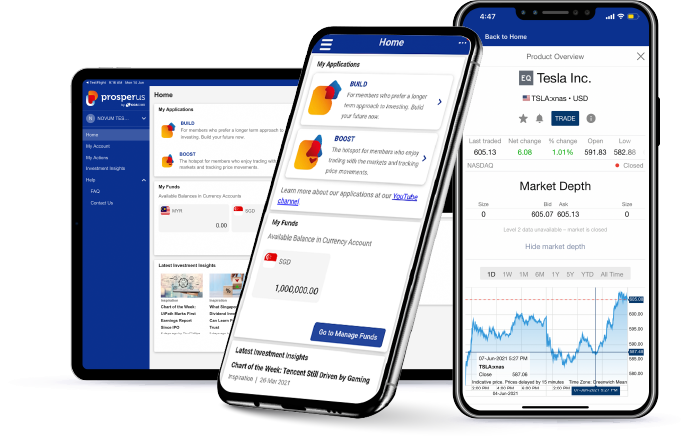

Start your investment journey with ProsperUs

Image credit: ProsperUs

Every new venture comes with its own learning curve. But as long as we do our due diligence and heed the advice of those who have gone before us, we can minimise the risks involved in things like investing.

To ease you into your investment journey, digital investment apps such as ProsperUs help newbies invest on-the-go with a user-friendly dashboard and portfolio pages – allowing you to view and keep track of your investment performance.

It’s even got crash courses for you to learn more about investing. Its educational articles and webinars cover terms you should know, and even what’s new in the world of investing.

Whether you’re looking to earn more income, or simply want to learn more about what investing can do for you, ProsperUs has the resources you need so you’ll start your journey like a seasoned investor.

TSL readers looking to start their own investment journey with ProsperUs can sign up with the code <TSL100>. There are attractive prizes to be won, like an iPhone 13 Pro and an exclusive martini tasting when you open up an account. As an added perk, get SGD$100 in cash credit after the completion of three trades on the platform.

Start investing with ProsperUs here

This post was brought to you by ProsperUs.

Photography by Doreen Fan.

This article is meant for information only and should not be relied upon as financial advice.

Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

This advertisement has not been reviewed by the Monetary Authority of Singapore.